Now that I have a toddler, one of my favorite things to do after she goes to sleep is veg out on the couch, browse Redfin, and dream of moving to a bigger house. Anyone else or is that just me?

A house came up in our neighborhood and I became slightly obsessed. They posted it a week before listing it as “coming soon.” The price gave me a bit of anxiety, as did the thought of moving in general, but I envisioned my daughter playing on the play structure in the backyard, being able to actually host people, and having adequate storage for all of our stuff. Oh so dreamy.

But then I began to wonder…. is it really only a dream or could it be reality?

So I plugged our financials into an online mortgage affordability calculator. According to this, technically, yes, we could afford this house. But something didn’t feel right.

Table of Contents

- Why Mortgage Calculators Don’t Tell the Full Story

- A Better Way to Think About Home Affordability

- What Happens When You Look at the Full Monthly Cost of Homeownership

- Stress Testing Your Budget

- The Takeaway: Affordability is More Than a Number

- A Simple Tool That Helped Me See the Full Picture

- Final Thoughts

- FAQs on Buying a Home

Why Mortgage Calculators Don’t Tell the Full Story

Most mortgage (affordability) calculators, and even lenders, are designed to answer one question:

“How much can you be approved for?”

But that is not the same as:

“How much can you comfortably afford in real life?”

Most online calculators base their estimates on gross income, ideal assumptions, and limited monthly expenses. They don’t account for how your budget actually works.

The Problem With Using Gross Income

When you use a typical mortgage calculator, it’s usually based on your gross income.

But your day-to-day life runs on your net (take-home) income; i.e., what you actually have to spend on your mortgage and everything else.

This gap matters more than many people realize.

What Gets Left Out of Most Affordability Calculations

This is where things start to break down.

Most tools don’t fully account for:

- Property Taxes

- Home Insurance (or PMI)

- Maintenance & Repairs

- HOA fees

- Utilities

- A realistic buffer for unexpected costs

All of the above impacts what you have left each month, on top of the gap between gross and net income.

A Better Way to Think About Home Affordability

Instead of asking: “How much house can I afford?”

Try asking: “What would this home actually feel like month-to-month?”

Affordability isn’t just about qualifying for a loan. Not at all. It’s about feeling financially stable, having breathing room, and not stretching yourself too thin.

What “Comfortable” Actually Looks Like

When you look at your full monthly picture, you start to see what feels comfortable, what feels tight, and where the tradeoffs are.

Some homes technically work, but leave you with very little flexibility.

Other homes may give you room to handle unexpected expenses without stress.

What Happens When You Look at the Full Monthly Cost of Homeownership

When I started layering in our net household income, the full monthly PITI payment, maintenance and utility buffers, and compared that to what we actually bring home each month, the numbers told a different story.

Some homes that seemed affordable at first didn’t feel that way anymore.

Stress Testing Your Budget

Another thing most calculators don’t show is what happens when things change.

For example, interest rates could increase, home prices could shift (or you end up in a bidding war and have to offer more than you intended), and unexpected expenses come up.

A home that feels manageable today can quickly feel tight under slightly different conditions.

The Takeaway: Affordability is More Than a Number

The biggest realization for me was this: Affordability isn’t just a number, it’s a feeling backed by numbers.

It’s not about how much you have, but how much you have left. It’s about how resilient your budget it and how confident you feel moving forward.

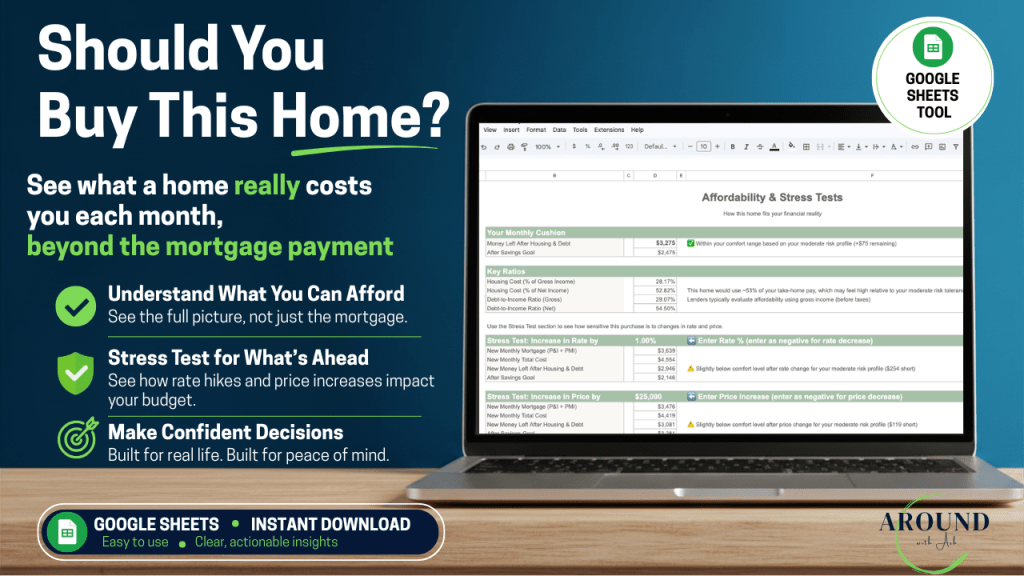

A Simple Tool That Helped Me See the Full Picture

If you know me, you know I am a spreadsheet geek. I love to make spreadsheets for everything. I’m also into real estate finance, it’s my day job. So I took it upon myself to create a mortgage affordability spreadsheet tool to help me see the big picture.

This tool looks at real monthly income, calculates total housing cost, shows what’s left over, and allows you to stress test to different situations.

It has made it much easier to understand what actually works, what’s pushing it, and what doesn’t make sense.

Lo and behold, we did not put an offer on this dreamy house, but all for the better because I wouldn’t be able to sleep at night knowing the full cost we would have been paying.

If you’re thinking about buying a home, whether you have one in mind or are just exploring your budget, this tool might help you too. Right now (at time of posting) it’s priced at “Pay What You Want.”

Final Thoughts

Buying a home is one of the biggest financial decisions you’ll make. You don’t need perfect certainty, but you do need clarity.

There’s a big difference between being approved for a number and feeling comfortable living with it.

FAQs on Buying a Home

Since I work in the industry, I thought it would be prudent to provide some further insight into common questions when it comes to home buying. Please note I am not an agent or a broker, and this should not be considered professional, financial, or legal advice. It’s simply meant to provide helpful context as you navigate your homebuying decision.

How much house can I really afford?

Most lenders and mortgage calculators estimate affordability based on your gross income and standard debt-to-income ratios. But what you can comfortably afford depends on your take-home (net) income, monthly expenses, and how much flexibility you want in your budget.

A more realistic approach is to look at your full monthly housing cost, what you’ll have left over, and how that fits into your day-to-day life.

Why do mortgage calculators say I can afford more than I expected?

Mortgage calculators, and really lenders, are designed to determine what you can be approved for, not necessarily what feels comfortable. They typically use gross income instead of net income, assume limited expenses, and don’t account for lifestyle or savings goals. That’s what the number can feel higher than expected. You should always aim to purchase a house for less than what you are approved for by a lender.

What is included in a true monthly housing cost?

Your monthly cost isn’t just your mortgage payment.

A more complete estimate includes:

- Principal and Interest

- Property Taxes

- Homeowners Insurance

- PMI (if applicable)

- HOA fees (if applicable)

- Maintenance & repair costs

- Utility costs

Looking at all of these together gives you a much clearer picture of affordability.

How much money should I have left after buying a home?

There is no one-size-fits-all number. Everyone’s situation is different, but it also depends on your lifestyle, goals, and risk tolerance.

A good rule of thumb is to make sure you still have enough for everyday expenses, room for savings and emergencies, and flexibility for unexpected costs. If your budget feels tight after housing, it may be a sign you’re stretching too far.

If you haven’t already tracked your expenses to see how much you spend outside of housing, I would highly recommend you do so. That way, you will know exactly how much money you need to have leftover after you new mortgage payment. I personally use Monarch Money for my personal finance tracking. If you want to give them a try, here’s my referral link to get 50% off your first year: Monarch Money 50% Off

If lenders base mortgage qualifications on gross income, shouldn’t I base my budget on gross income, too?

No. No no no. For real-life affordability, net income is much more useful. The tool I made includes ratios based on gross income so you can see what the lenders see, but your decisioning should always be made on net income. You will always have to pay taxes, you are not getting that money back. Sure, you could adjust your medical or 401(k) deductions, but ideally you wouldn’t have to. Your housing decision should be based on what you actually bring home.

What happens if interest rates increase after I buy?

If you have a fixed-rate mortgage, your principal and interest payment won’t change. A 30-year fixed-rate mortgage is the common bread-and-butter of mortgages. If you are interested in an ARM (adjustable-rate mortgage), your lender will provide you more details on how frequently and when your rate will change.

Even though your rate is fixed and your principal & interest costs won’t change, your total monthly cost can still increase over time due to rising property taxes, insurance changes, and of course repairs/utilities.

That’s why it’s important to leave room in your budget, and not just plan for today’s numbers.

Discover more from Around with Ash

Subscribe to get the latest posts sent to your email.